The 2 Best Ways To Invest In Tech Right Now

Outside of the revitalized energy patch, no corner of the U.S. economy is hotter than Silicon Valley.

Google (Nasdaq: GOOG), the region’s bellwhether, has tacked on a 50% gain over the past 12 months, adding more than $100 billion its market value. #-ad_banner-#

And moving far down the tech food chain, the hottest young tech companies are also creating great wealth for their employees and shareholders: Recent IPOs RocketFuel (Nasdaq: FUEL) and FireEye (Nasdaq: FEYE) have more than doubled since their IPOs last month. These companies are boosting sales at a really fast pace, but they’ve also quickly become richly valued. For instance, FireEye is valued at $4.7 billion but is expected to have just $230 million in sales in 2014.

On the other end of the tech investing spectrum are some deep value plays. But in cases like IBM (NYSE: IBM), growth will be so limited that they are really more like value traps.

Simply put, in the world of tech, you can have growth or value, but not both.

But a few companies stand out for a reasonable measure of both growth and value. Each company is in the midst of near-term headwinds that are dampening 2013 profit growth, but each has a catalyst that could help them regain favor in 2014.

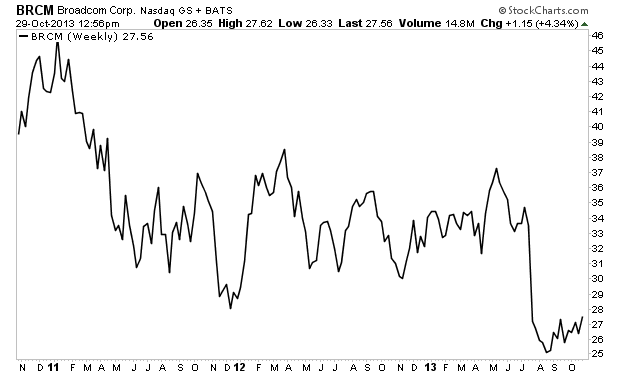

| 1. Broadcom (Nasdaq: BRCM ) |

This maker of communications chips was a growth juggernaut in the past decade, as sales rose from $2.7 billion in 2006 to $6.8 billion in 2010. Since then, growth has sputtered, as sales rose less than 10% in 2011 and 2012, and are likely to grow less than 5% this year and the first half of 2014. This maker of communications chips was a growth juggernaut in the past decade, as sales rose from $2.7 billion in 2006 to $6.8 billion in 2010. Since then, growth has sputtered, as sales rose less than 10% in 2011 and 2012, and are likely to grow less than 5% this year and the first half of 2014. What went wrong? Broadcom has failed to keep up with rivals such as Qualcomm (Nasdaq: QCOM) in the area of wireless chips, which set the stage for especially weak near-term sales guidance. As a result, this stock now trades near multi-year lows.

Yet investors are being too myopic, focusing on likely weak results over the next few quarters, and should instead be focusing on the next few years. One of the key drivers for Broadcom will be a growing rollout of advanced telecom networks, known as LTE (Long-Term Evolution). Broadcom recently acquired the wireless division of Renesas, which won’t enable it to overtake Qualcomm in the wireless baseband segment but should help it act as a second source provider with the wireless service providers that typically split contracts for key components among two vendors. Right now, investors are assuming that Broadcom will show little traction with this effort. Assuming a worst-case scenario, analysts at Morgan Stanley have put aside the wireless business and believe the rest of the business is worth $31 a share, roughly 20% above the current price. And what if Broadcom gains traction in LTE? If the company secures “LTE wins in (the second half of 2014) with major customers, and maintains dominant share of connectivity,” then shares will trade up to $42, according to these analysts. Outside of wireless, Broadcom’s industry presence remains impressive. The company is a leading provider of chips that go into broadband networks and other parts of the telecom infrastructure. And it’s a very profitable business: Annual free cash flow is likely to keep exceeding $1.5 billion despite the near-term challenges. Still, the real upside for this stock will only come with LTE traction. “While we believe BRCM is very well-positioned in many of its markets, particularly in attractive margin areas such as infrastructure networking and broadband, the firm’s fate in mobile and wireless is still up in the air,” said Cody Acree, director of research at Williams Capital. That said, “We do believe this could be an attractive entry point for long-term investors, as the announcement of 4G (LTE) wins over the next few months could be a driver of share appreciation.” Their $35 price target is 30% above current levels. The key takeaway: Shares hold solid support at current levels and would possess solid upside if Broadcom can reinvigorate the wireless business. |

| 2. EMC (NYSE: EMC ) |

This company remains as a clear leader in the field of data storage, but its shares have failed to keep up with broader market as pricing pressures have crimped margins by a few basis points. This company remains as a clear leader in the field of data storage, but its shares have failed to keep up with broader market as pricing pressures have crimped margins by a few basis points. As a result, this is one of the cheapest tech stocks you’ll find. “EMC’s (enterprise value to free cash flow) multiple has contracted to 8x, roughly near the bottom post-crisis. That’s close to where (Hewlett-Packard (NYSE: HPQ)) and Apple (Nasdaq: AAPL) trade and well below IBM,” note analysts at UBS.

Yet the valuation is even more appealing when you take into account EMC’s 80% stake in VMWare (NYSE: VMW). Then, the enterprise value to free cash flow multiple moves below 7, according to UBS (which means that the free cash flow yield is above 13%). Most cheap tech stocks deserve their low multiples simply because they have the wrong business models for these times. But EMC is at the center of one the biggest trends: cloud computing. “We consider EMC among the better positioned large vendors with moderate storage growth, ownership of VMware, and a Big Data option in Pivotal,” write the UBS analysts, who have a $30 price target, roughly 20% above current levels. Yet they think shares could also move up to $35, if Pivotal, which was formed by EMC and VMW earlier this year, gains real traction. (You can read more about Pivotal here.) |

Risks to Consider: The broader Nasdaq has moved well higher the past few years, and any correction into this group would make it hard for Broadcom or EMC to rally.

Action to Take –> The key takeaway: Just like Broadcom, shares of EMC possess solid support at current levels with moderate upside. And each firm is pursuing a growth initiative that could yield much more upside.

P.S. The future looks bright for Broadcom and EMC, but for a couple of next year’s top tech plays, check out our latest report, “The Hottest Investment Opportunities of 2014.” In it, you’ll learn about how Apple could threaten the banking industry and how the “death of the keyboard” could mean huge growth for one tiny company. For more information, click here now.