Digesting The Latest Inflation Numbers… Plus: One Way To Escape Inflation (And The Taxman)

You’ve probably seen the news by now. And if you’ve been following along with us for a while, it shouldn’t come as any big shock.

Inflation remains persistently high. Yesterday, the The Labor Department released its consumer price index (CPI) reading for September.

Overall CPI rose 0.4% from August and was up 8.2% on a year-over-year basis in September.

Source: Statista

That’s down from 8.3% in August, but overshot expectations of 8.1%.

In other words, prices remain near 40-year highs.

Core CPI, which excludes volatile food and energy prices, rose 6.6% year over year. That’s the highest pace since 1982.

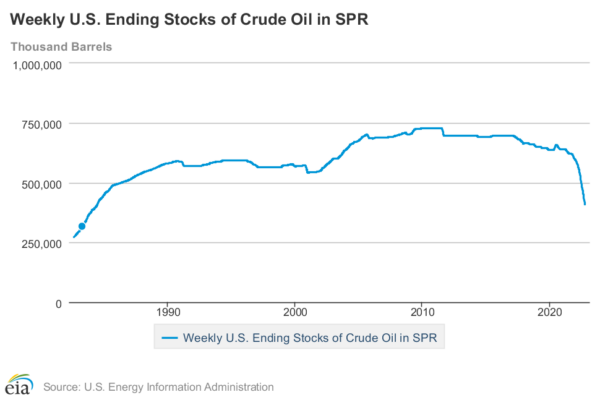

While items such as car prices and gas prices have gone down, those were offset by increases in housing, food, and healthcare. And as a side note, I wouldn’t get too comfortable with those lower gas prices either. With the recent OPEC+ decision to cut oil production, we’re already seeing gas prices creep back up. (And releasing reserves from the Strategic Petroleum Reserve won’t be an option this time — as my colleague Robert Rapier recently noted, the SPR is now at its lowest level since 1984.)

All of that to say, any hopes of a “pivot” by the Federal Reserve are dead in the water right now. So get ready for another interest rate hike of 0.75% when the Fed meets next month. And as things look right now, it’s looking like the voting members may not get their preferred slowdown rate hike of 0.5% in December (as indicated by the previous “dot plot”).

However, rather than dwell on this, I want to focus on solutions. And that’s why I’m turning things over to my colleague Nathan Slaughter today. Below, he builds off of a previous article touting the virtues of municipal bonds — and why they make a lot of sense right now.

Enjoy,

Brad Briggs

StreetAuthority Insider

Escape The Taxman (And Inflation) With One Of The Safest Asset Classes Around…

Earlier this week, I pointed out that the U.S. Treasury Department reported an alarming statistic.

Earlier this week, I pointed out that the U.S. Treasury Department reported an alarming statistic.

The U.S. national debt has surpassed $31 trillion.

As I mentioned, it doesn’t look like this number is going to slow down anytime soon. And that can only mean one thing… your taxes are going to go up.

In that piece, I wrote about a potential solution for investors who want to keep more of their hard-earned money out of Uncle Sam’s hands: municipal bonds.

Today, I’d like to talk more about this “boring” but wonderful asset class — and why you should consider adding a little exposure to your portfolio. (I’ll even tell you about one of my favorite ways to invest…)

The Tax Man (Almost) Always Comes

As a refresher, when states, cities, and other agencies need to raise money for public works (think new roads, bridges, schools, hospitals, water treatment plants, etc.), they will issue debt in the form of a municipal bond.

Not only are bonds among the safest investments around, but the income they pay is generally exempt from federal income taxes (and often state and local taxes).

Here’s why that’s makes them so appealing, particularly for higher-earning investors…

If you do your taxes yourself, then you may know that investors must report any taxable interest income earned on line 2B on the 1040 return.

If you’re in the 37% tax bracket, then 37 cents from every dollar of interest earned in a taxable account goes to Uncle Sam. So for every $10,000 earned during the year, you need to cough up $3,700 on April 15, keeping just $6,300.

And that’s before we even get into the net investment income tax (NIIT). If your modified adjusted gross income is $200,000 or greater for single-filers or $250,000 and married filing jointly, you’ll owe an additional 3.8%.

It doesn’t matter if we’re talking about a savings account or a corporate bond ETF. Virtually every fixed-income investor must return a portion of their earnings each year. Even government bond funds don’t give investors any relief at the federal level.

That’s where municipal bonds can help. They keep the taxman out of your pocket, while also reducing your exposure to market volatility.

Do The Math…

To see how this can work in your favor, let’s consider this scenario involving two bonds:

— Texas Transportation Comm. Highway Bonds, AAA-rated, maturing April 2025 with a 4.3% current yield

— Goldman Sachs notes rated ‘A’ maturing Jan 2024 with a current yield of 5.4%

Which would you choose?

The Goldman Sachs bond pays out $54 for every $1,000 invested, versus $43 for the Texas muni. But for upper-income investors, that pre-tax income of $54 suddenly becomes an after-tax income of $31.97 (37% tax rate, plus 3.8% NIIT). And that’s even less if state and/or local taxes are a factor.

But you owe nothing on the Texas bond. As a municipal agency, the interest it pays is untouchable. I think we’d all rather earn $43 than $34. So on an after-tax basis, the muni bond is clearly superior to the taxable bond.

The question is, by how much? That’s actually pretty simple to figure out using the formula I shared in my previous article.

Tax-Equivalent Yield = Muni Yield / (1 – Your Federal Tax Bracket)

If we plug in the numbers, then it looks like this:

4.30 / (1 – 0.408) = 7.26%.

In other words, if you started with a rate of 7.26% and surrendered 37% of the income to taxes, plus 3.8% in net investment income taxes, then you would be left with the same 4.3% offered by the Texas muni. Therefore, it is said to have a tax-equivalent yield of 7.26%.

In essence, this is what a taxable bond would need to yield to match the payout on the tax-free bond. Or, from another perspective, the difference in quoted yield and tax-equivalent yield represents the muni’s tax savings to investors.

My Preferred Way To Invest In Munis

The appeal of munis is clear. And like I mentioned in my previous piece, I think munis are offering investors a deal right now. That’s because they’ve sold off considerably, thanks to rising interest rates.

I’ll admit it… I’m not a bond buy. So rather than pick and choose (as well as for diversification), I recommend leaving that job to the pros and choosing a muni bond fund.

That’s why Eaton Vance Muni Income (NYSE: EVN), a closed-end fund, is one of my top picks for investors who want exposure.

Thanks to rising rates, EVN has lost 27% in 2022, which is crazy considering we’re talking about the municipal bond market. The pullback has little to do with declining credit quality, rising defaults, or other fund-specific factors. In fact, EVN continues to rate five stars from Morningstar and the hand-picked portfolio spans more than 300 “A”, “AA”, and “AAA” rated issues. Many of these are revenue bonds tied to the construction of toll roads, hospitals, and water and sewer infrastructure projects.

While the Fed’s rate tightening presents short-term headwinds, municipal bankruptcy filings are exceedingly rare — even when the economy is sluggish. And thanks to the recent dip, EVN’s payout has increased to about 5%.

Here’s math works out for those in the 37% tax bracket:

37% + 3.8% NIIT = 40.8%

5% / (1 – 0.408) = 8.44%.

Again, that’s what a taxable bond fund would need to yield to match this tax-free payout.

Closing Thoughts

As mentioned earlier, muni bonds can be an excellent way to lower your tax liability and keep more of what you earn. The higher your tax bracket, the more valuable they can be.

What’s more, closed-end funds like EVN can trade at a discount to their net asset value (NAV). In EVN’s case, it’s trading at an 11% discount (historically, it usually trades at a 6% discount) — so you’re getting even more bang for your buck here.

As always, you should do your own research in this space before deciding what’s right for you. But with persistently high inflation and the prospect of tax hikes on the horizon, EVN is a compelling option for anyone seeking steady, tax-exempt monthly income.

In the meantime, if you’d like to get your hands on my absolute favorite picks, then you need to check out my latest report…

I recently revealed my 5 favorite “bulletproof” high-yield stocks to own right now. Each one has weathered every dip and crash over the last 20 years and STILL handed out massive gains.

With picks like these, you may never have to worry about what the market is doing again… Go here to learn more now.